> For the complete documentation index, see [llms.txt](https://docs.siren.xyz/llms.txt). Markdown versions of documentation pages are available by appending `.md` to page URLs; this page is available as [Markdown](https://docs.siren.xyz/siren-protocol/siren-flow-architecture/automated-hedging-system.md).

# Automated Hedging System

Siren Flow’s vaults incorporate an automated hedging system that protects liquidity providers from delta exposure by interacting with Arbitrum-based perpetual protocols like [Perennial](https://twitter.com/perenniallabs?lang=en). This advanced feature ensures that LPs’ returns remain uncorrelated with market movements. By integrating automatic delta-hedging of pool exposure with perpetual and DEX protocols, Siren Flow provides LPs with yield opportunities that are insulated from the volatility of crypto markets.

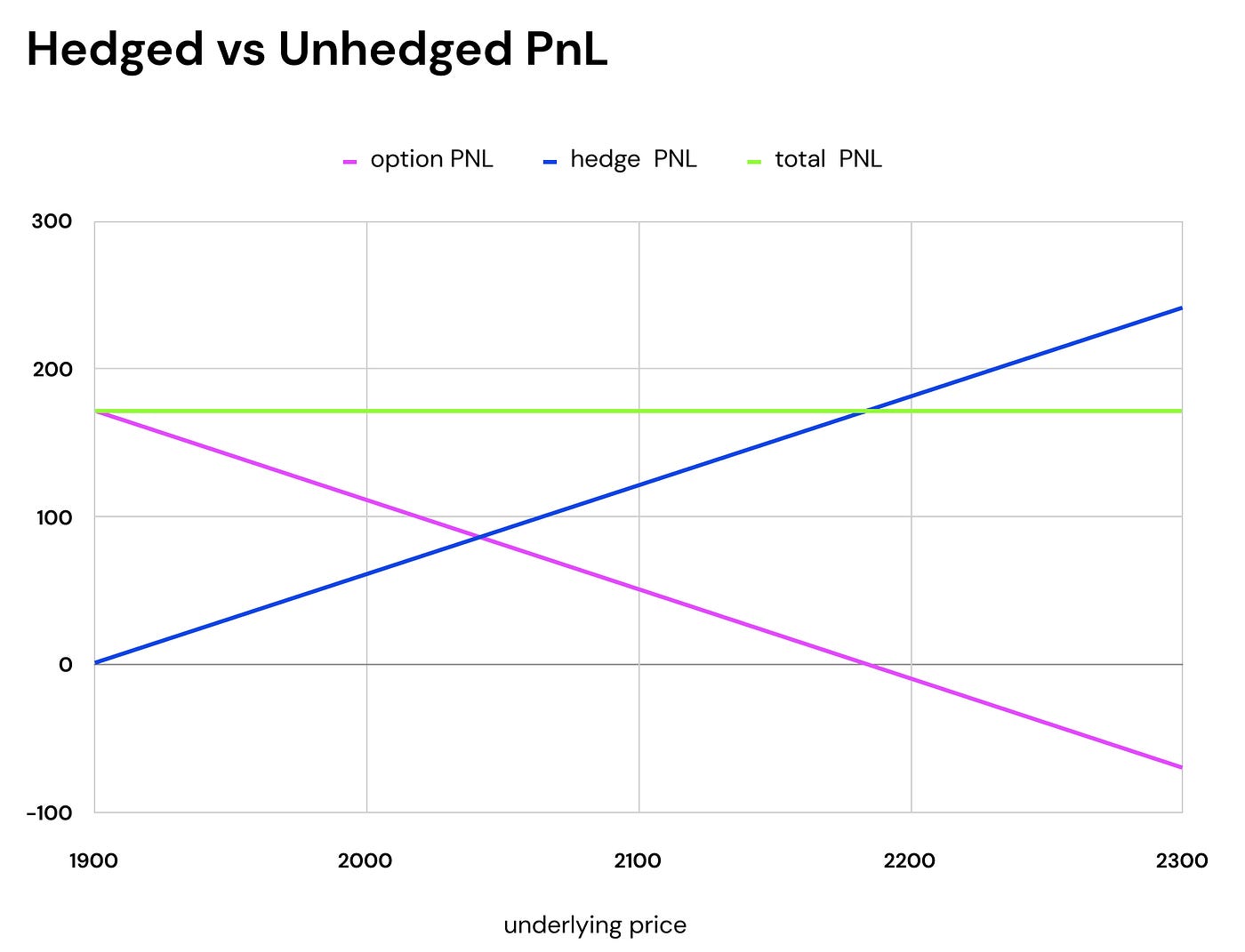

Above is a comparison of hedged vs unhedged profit-loss (PnL) of a short call option position with strike price of 2,000. The writer initially receives $175 from selling the options to the trader. As the price of the underlying asset rises, the option increases in value, resulting in projected losses for the writer (pink line).

To hedge their delta exposure, the seller can purchase a perpetual contract and update it frequently to match option delta Δ (blue line). In this example, the hedge is updated every $10 move in price. As the option increases in value, creating losses for the writer, the corresponding perpetual position profits proportionally. The green line represents combined PnL — as we can see, it enables the seller to decouple their return from the market price movements and protect their initial premium received.

These hedged positions are created and maintained by the Hedge Keeper, an off-chain module that can connect to many different perpetual protocols and DEXs. Similarly to how having the Quote Provider off chain allows pricing to be responsive, moving the Hedge Keeper off chain allows it to calculate the hedge proactively, in advance of the latest asset price being known on chain. This advantage has the potential to increase the accuracy of the hedge, improving LP yields.

Liquidity providers on Siren Flow do not seek directional exposure to the underlying price; instead, they earn yield from facilitating markets for traders through automated delta hedging.

*NOTE: This is a living document that will continue to be updated as Siren evolves. To contribute, please visit* [*Siren on GitHub*](https://github.com/sirenmarkets/core)*. Specific questions may be answered and technical guidance may also be provided from time to time in the* [*Siren Discord*](https://discord.gg/sirenxyz) *to those who are interested in building on top of the protocol.*

---

# Agent Instructions

This documentation is published with GitBook. GitBook is the documentation platform designed so that both humans and AI agents can read, navigate, and reason over technical content effectively. Learn more at gitbook.com.

## Querying This Documentation

If you need additional information that is not directly available in this page, you can query the documentation dynamically by asking a question.

Perform an HTTP GET request on the current page URL with the `ask` query parameter, and the optional `goal` query parameter:

```

GET https://docs.siren.xyz/siren-protocol/siren-flow-architecture/automated-hedging-system.md?ask=&goal=

```

`ask` is the immediate question: it should be specific, self-contained, and written in natural language.

`goal` is optional and describes the broader end goal you are ultimately trying to accomplish on behalf of the user. GitBook uses it to tailor the answer towards what is most useful for that goal.

The response will contain a direct answer to the question and relevant excerpts and sources from the documentation.

Use this mechanism when the answer is not explicitly present in the current page, you need clarification or additional context, or you want to retrieve related documentation sections.