> For the complete documentation index, see [llms.txt](https://docs.siren.xyz/llms.txt). Markdown versions of documentation pages are available by appending `.md` to page URLs; this page is available as [Markdown](https://docs.siren.xyz/siren-protocol/siren-flow-architecture/hybrid-pricing-model.md).

# Hybrid Pricing Model

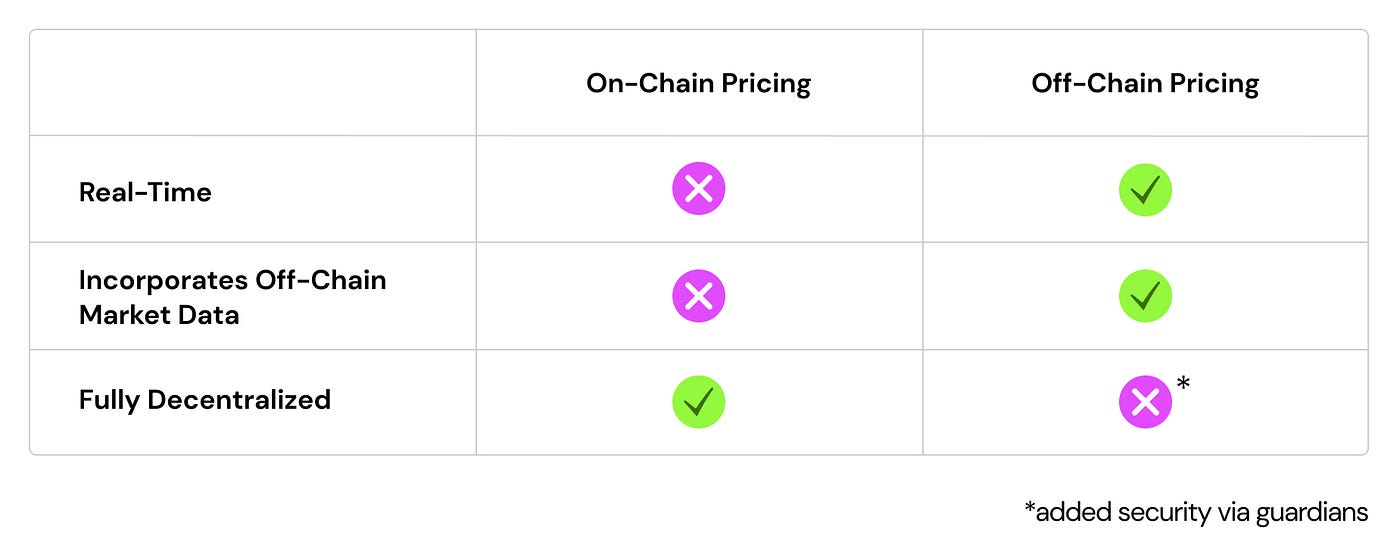

Siren Flow employs a unique hybrid on-chain/off-chain RFQ system to deliver competitive pricing for options trades. This innovation allows Siren Flow to offer pricing comparable to centralized exchange derivatives while retaining the benefits of self-custody and decentralized trading. The hybrid pricing model combines on-chain execution with off-chain quote generation, paving the way for more sophisticated protocol elements. This ensures traders no longer have to choose between security and competitive pricing, as they can have both with Siren Flow.

In Siren Flow, prices are not calculated on-chain. Instead, price generation for trades is delegated to Quote Providers. Quote Providers are specialized off-chain services that maintain an internal volatility surface, which incorporates both on-chain and off-chain data to provide competitive real-time price quotes.

For the initial Siren Flow testnet and launch, the protocol will use Quote Providers created by the Siren Team. In the future, Siren Flow plans to connect to other pricing providers, such as [Sommelier](https://twitter.com/sommfinance), to expand its access to data and generate even more competitive and accurate pricing. This feature will further enhance Siren Flow’s value proposition and increase the benefits for traders and LPs.

When users perform trades on Siren Flow, they ask the Quote Provider API to generate a cryptographically signed order containing one or more options trades (legs). The order specifies the premium paid or received for each leg of the order. Traders can execute the order by submitting a transaction on chain, which is instantly settled. After the settlement, options tokens are sent to the trader’s wallet.

Order structure:

To mitigate the risk of having the RFQ system off-chain, each order is co-signed by Guardians to prevent malicious orders from being settled against a pool.

*NOTE: This is a living document that will continue to be updated as Siren evolves. To contribute, please visit* [*Siren on GitHub*](https://github.com/sirenmarkets/core)*. Specific questions may be answered and technical guidance may also be provided from time to time in the* [*Siren Discord*](https://discord.gg/sirenxyz) *to those who are interested in building on top of the protocol.*

---

# Agent Instructions

This documentation is published with GitBook. GitBook is the documentation platform designed so that both humans and AI agents can read, navigate, and reason over technical content effectively. Learn more at gitbook.com.

## Querying This Documentation

If you need additional information that is not directly available in this page, you can query the documentation dynamically by asking a question.

Perform an HTTP GET request on the current page URL with the `ask` query parameter:

```

GET https://docs.siren.xyz/siren-protocol/siren-flow-architecture/hybrid-pricing-model.md?ask=

```

The question should be specific, self-contained, and written in natural language.

The response will contain a direct answer to the question and relevant excerpts and sources from the documentation.

Use this mechanism when the answer is not explicitly present in the current page, you need clarification or additional context, or you want to retrieve related documentation sections.